Dubai Real Estate Market Update – July 2025

Dubai’s real estate market continues to defy expectations, pushing to new highs in July 2025. The emirate witnessed a strong combination of price growth, record transaction volumes, and a flood of new project launches. However, beneath the surface, signs of cooling momentum and buyer fatigue are also emerging, signaling a more selective and value-driven phase ahead.

In this detailed update, we explore the key trends, price movements, transaction activity, mortgage dynamics, and developer launches that shaped the property market in July 2025.

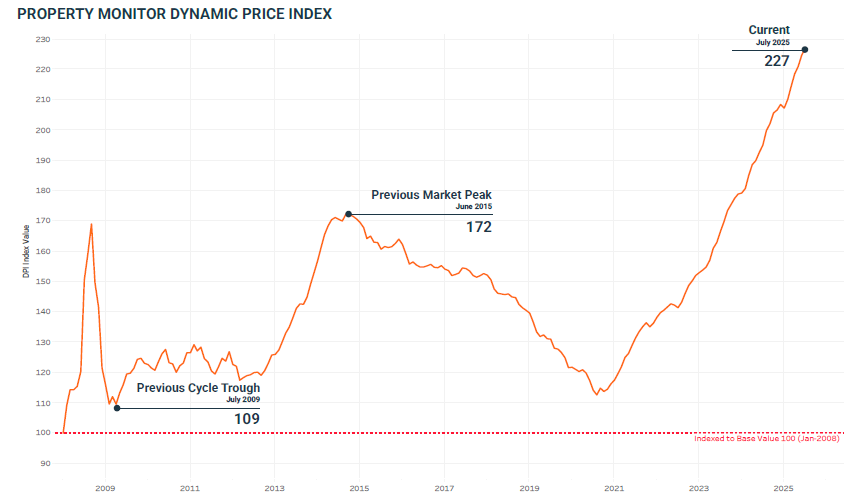

Property Prices – A Continued Climb

According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices rose by 0.99% month-on-month, bringing the average price to AED 1,625 per sq. ft. This is a significant milestone, as prices now stand:

➡️31.7% above the 2014 peak

➡️99.5% above the October 2020 market trough

While price increases remain steady, the pace has moderated compared to June’s 1.71% growth. This signals a more measured climb, with apartments showing signs of softening while villas and townhouses continue to attract strong demand.

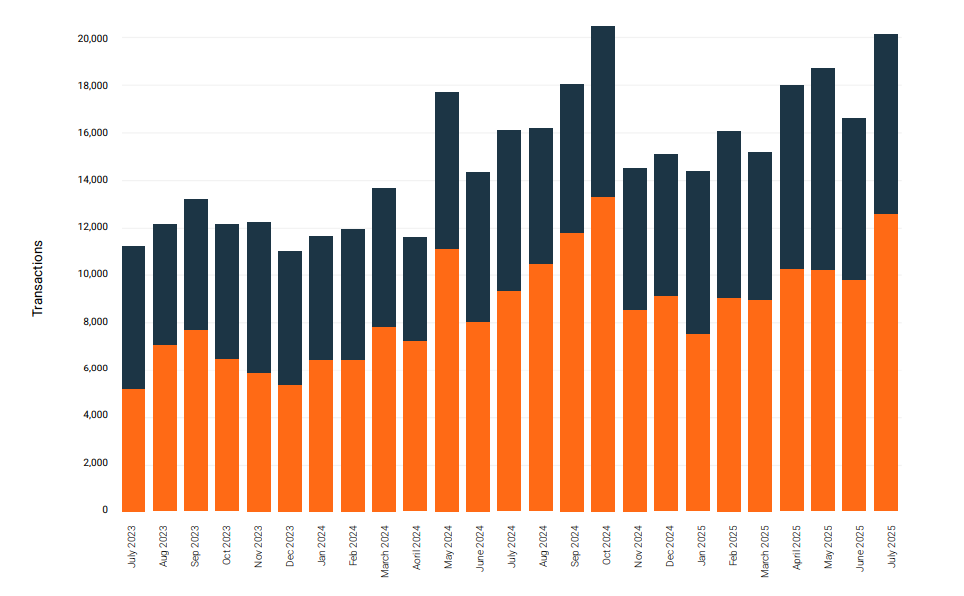

Record Transaction Volumes

Dubai’s property market continues its record-breaking run. 20,116 sale transactions were recorded in July, representing a 21.3% increase from June.

Key highlights:

➡️Residential properties (apartments, villas, townhouses) dominated with 93.7% of sales.

➡️Commercial assets such as offices, vacant land, hotel apartments, and retail spaces accounted for the remainder.

➡️Year-to-date, Dubai has recorded over 119,000 transactions, up 23% compared to 2024.

At this pace, Dubai is on track to surpass 200,000 annual transactions, setting a new all-time record by year-end.

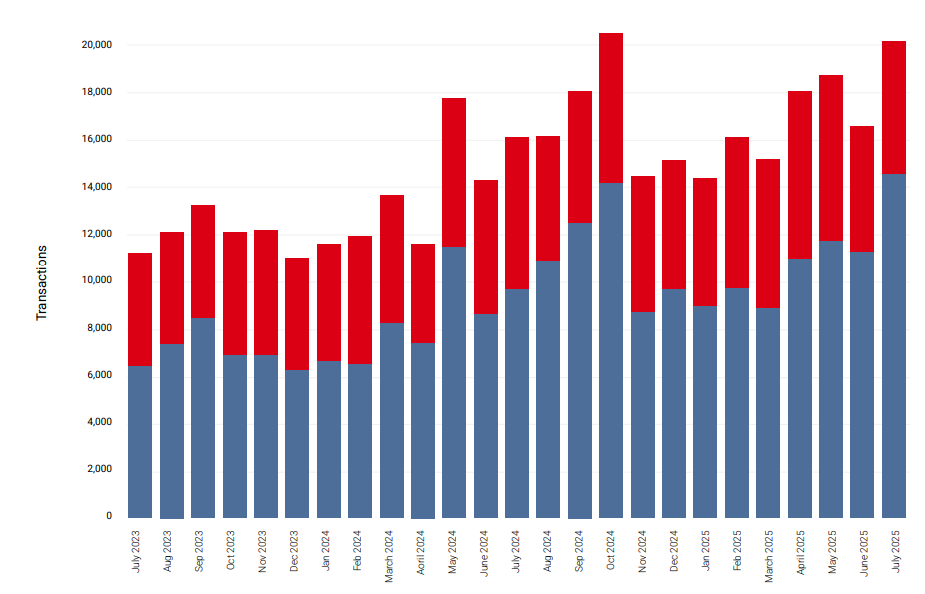

Off-Plan vs. Resale Dynamics

The off-plan segment continues to dominate:

➡️12,595 Oqood transactions were recorded in July, up 28.3% month-on-month.

➡️Adjusted for technicalities, off-plan transactions represented 72.1% of the market share.

➡️Resale activity declined to 27.7% of the market, reflecting a 5.2% monthly drop.

This trend suggests that buyers are favoring direct developer deals, driven by attractive incentives and flexible payment plans. Resale listings—often priced at a premium—are facing tougher competition, forcing investors to recalibrate expectations.

New Project Launches – Flood of Supply

Dubai’s developers remained aggressive in July, with over 50 new launches introducing 13,800 units valued at AED 38 billion.

Year-to-date:

➡️Nearly 93,000 units launched

➡️AED 270 billion in estimated sales value

Notably, apartments made up 95% of new supply, while villas and townhouses accounted for just 2.5% each.

However, this surge is testing market depth. Unlike previous years where launches sold out within hours, today’s projects are taking longer to move. Buyers are more selective, prioritizing value, differentiation, and long-term viability over hype.

Mortgage Market – Record Lending Activity

Mortgage activity reached a new high in July:

➡️4,891 loans issued (+9.2% MoM)

➡️45.6% were purchase mortgages with an average loan size of AED 1.8 million

➡️Loan-to-value (LTV) ratios averaged 73.7%, slightly lower than historical norms

While new mortgages are booming, lower LTV ratios indicate increasing affordability pressures. Buyers must commit more upfront cash, yet the strong demand suggests a well-capitalized pool of end-users and investors.

Refinancing and equity release loans also grew, reflecting homeowners’ desire to tap into rising property values.

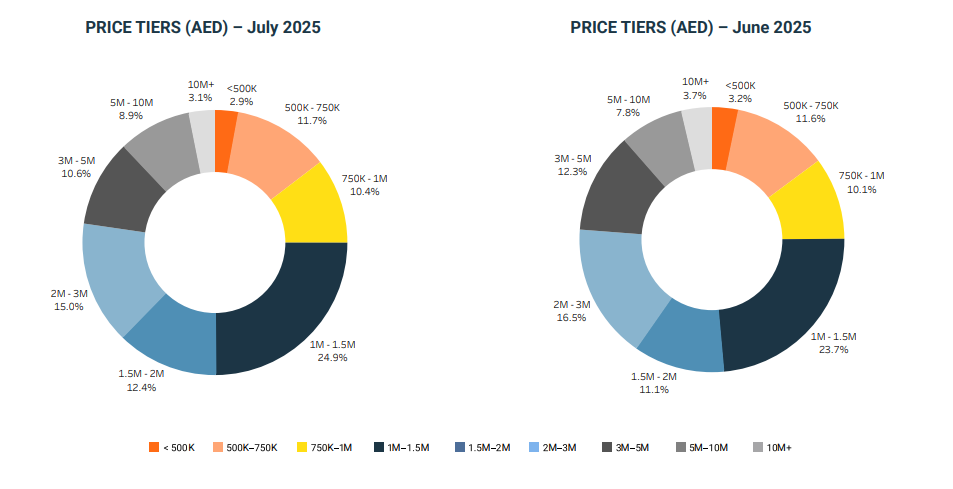

Market Segmentation – Price Tiers

Market activity by price tiers in July 2025 shows a shift toward mid-income and affordable segments:

➡️AED 1.5M–2M tier grew by 1.3%, reaching 12.4% market share.

➡️AED 1M–1.5M tier grew by 1.2%, now 24.9% of the market.

➡️High-end properties (AED 3M–5M) dropped by 1.6%, reflecting softer demand for luxury.

Condensed into three groups:

➡️Mid-tier (AED 1M–3M) → 52.3% of the market

➡️Affordable (AED 3M) → 22.7%

This breakdown underscores Dubai’s growing emphasis on functional, value-driven housing over speculative luxury.

Community Trends

Some of the most active master communities in July were:

➡️Jumeirah Village Circle (JVC) → 1,247 initial sales, with AKA Residence leading.

➡️Business Bay → 953 initial sales, driven by Binghatti Skyrise.

➡️DAMAC Riverside → 781 sales, with Indigo 2 leading activity.

For resales:

➡️JVC dominated again with 11.2% share.

➡️Business Bay followed at 6.4%.

➡️Dubai Marina ranked third with 4.5%.

These communities remain hotspots due to their strategic locations, mid-market pricing, and lifestyle appeal.

Market Outlook for H2 2025

Dubai’s property market remains fundamentally strong, but signs of strain are evident:

➡️Supply surge: Nearly 93,000 units launched YTD is testing demand.

➡️Buyer selectivity: Purchasers are more cautious, comparing projects carefully.

➡️Mortgage affordability: Rising upfront costs may moderate future demand.

➡️Price trajectory: Growth is expected to continue, but at a slower, more volatile pace.

Ultimately, the second half of 2025 will hinge on developers’ ability to differentiate their projects, align with end-user needs, and balance pricing with value.

July 2025 underscored Dubai’s position as one of the world’s most active property markets. With record-breaking sales volumes, steady price growth, and massive developer launches, the emirate continues to attract investors and homebuyers alike.

Yet, the market is maturing. Buyers are more discerning, affordability is under pressure, and project launches face tougher competition. As the year progresses, Dubai’s real estate landscape is likely to shift from a hype-driven market to a value-focused one, rewarding projects and communities that deliver genuine lifestyle and investment advantages.

For investors, developers, and end-users alike, the coming months will be pivotal in shaping the next phase of Dubai’s property cycle.