October marked the first non-record month of 2025, yet Dubai’s residential real estate market continues to show strong momentum. Here’s a detailed overview:

1. Price Growth Remains Steady

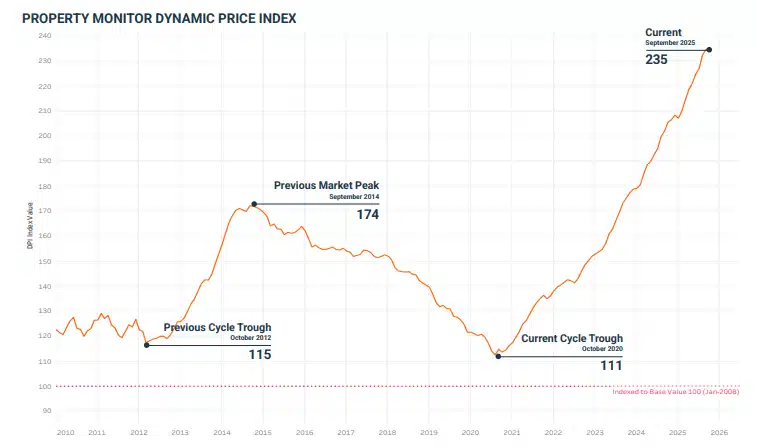

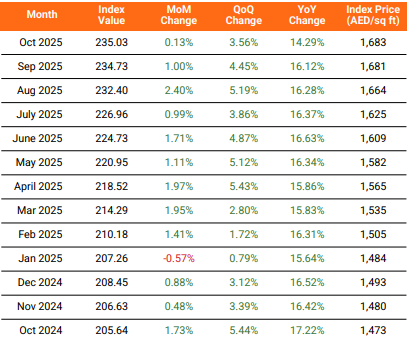

- Residential property prices grew by 0.13% in October, easing from the higher gains seen in September and August.

- The Property Monitor Dynamic Price Index (DPI) places average prices at AED 1,683 per sq ft, more than double the October 2020 low.

- Despite slower monthly gains, the long-term upward trend remains intact, supported by strong fundamentals.

2. Sales Activity

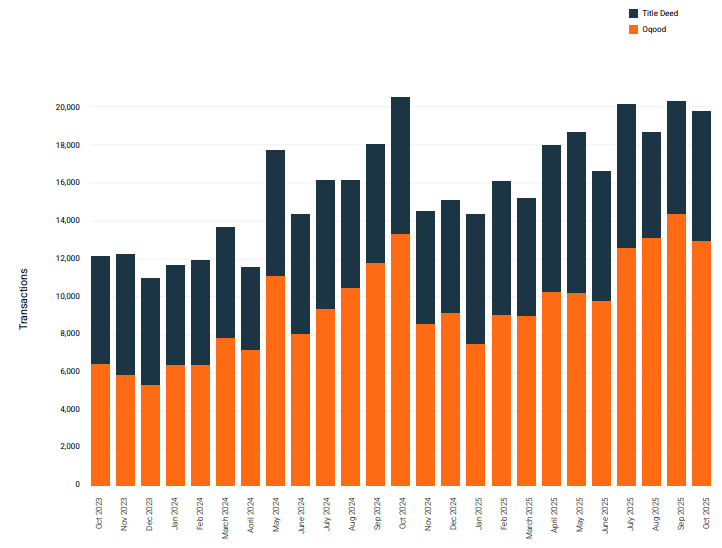

- A total of 19,760 transactions were recorded in October, marking the first year-on-year decline of 2025.

- October remains the second-strongest October on record, surpassed only by October 2024.

- Residential transactions accounted for 93.5% of all sales, with commercial activity dominated by office spaces (2.5%) and retail units (0.9%).

- Year-to-date (YTD) transactions have reached nearly 178,000, already surpassing 98% of 2024’s full-year total.

DPI MONTHLY OVERVIEW

3. Off-Plan vs Completed Properties

- Off-plan transactions (Oqood) accounted for 12,947 sales in October, down 9.9% from the previous month.

- After adjusting for technical classifications, the true off-plan market share stands at 70.6%.

- Title Deed transactions rose sharply by 14.7% month-on-month, mainly driven by completed apartment sales.

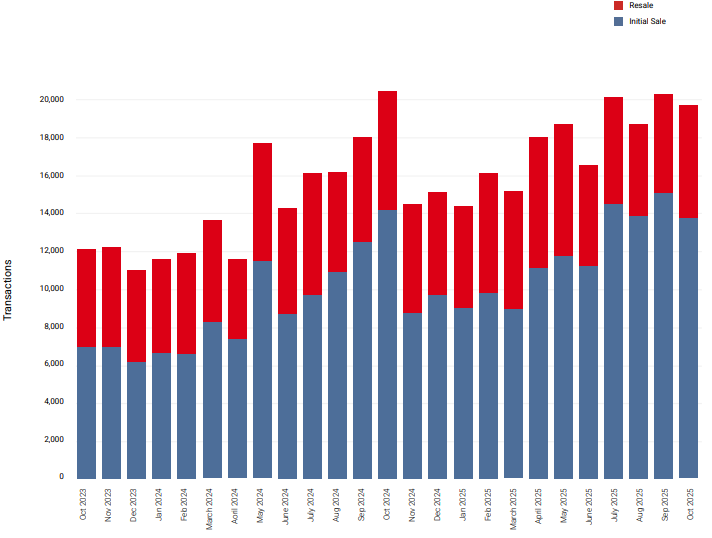

4. Resale Transactions

- Resales totaled 5,956 in October, up 4.6% month-on-month, representing 30.1% of the market.

- Off-plan resales contributed 21.7% of resale activity, with the 12-month rolling average at 25.1%.

HISTORICAL TRANSACTIONS – REGISTRATION TYPE TRANSACTIONS

HISTORICAL TRANSACTIONS – SALES RECURRENCE

5. New Project Launches

- 65 new projects launched in October, introducing over 14,000 residential units valued at AED 33.5 billion.

- YTD, 532 projects have been launched, adding 131,504 units—far exceeding a typical full-year pipeline.

- Apartments dominated launches at 99%, while villas and townhouses accounted for a smaller share.

6. Mortgage Activity

- Mortgage registrations rebounded by 28.9%, reaching 4,885 loans in October.

- New purchase mortgages accounted for 58.3% of transactions, with an average loan size of AED 1.79 million and LTV of 73.6%.

- Bulk mortgages surged 15.7% to 21.6% of total activity, reflecting renewed institutional buyer interest.

7. Popular Communities

- Jumeirah Village Circle led in initial sales (8.17%), followed by Jumeirah Village Triangle (6.6%) and Dubai Science Park (5.9%).

- In resale transactions, Jumeirah Village Circle also topped the chart (10.2%), followed by Business Bay (6.6%) and Dubai Marina (3.9%).

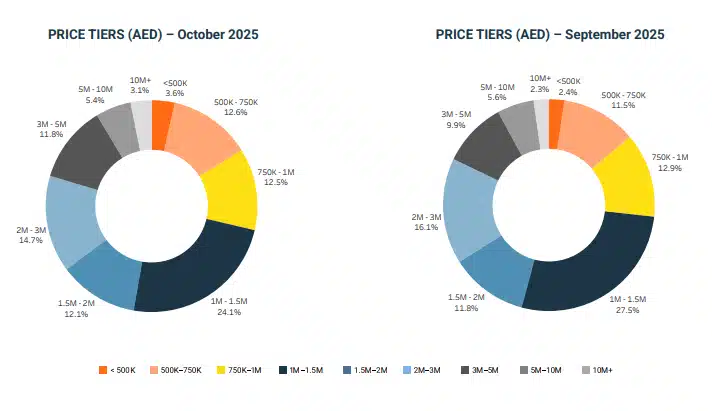

8. Market Segments & Price Tiers

- Mid-tier properties (AED 1M–3M) held the largest market share at 50.9%.

- Low-tier properties (<AED 1M) increased to 28.7%, while high-end properties (>AED 3M) grew to 20.4%.

- Growth was notable in both lower-mid and high-end segments, driven by off-plan and premium apartment launches.

9. Market Outlook

- Market conditions show measured normalization, with slower monthly gains but strong underlying fundamentals.

- Continued population inflows, economic resilience, and Dubai’s position as a global investment hub support long-term stability.

- The market is poised for sustained growth into 2026, with developers focusing on strategic launches and buyers remaining selective.